Over the years, we have discussed various constraints limiting financial inclusion whose targets were established in the 2012 National Financial Inclusion Strategy (NFIS). One of the critical inhibitors — access to financial access points through agents — was often pitched against the progress in other markets where telcos operate mobile money services. While the direct participation of telcos in Nigeria’s mobile money licensing regime was restricted, the Central Bank, after years of consultation and engagement is exploring a new mechanism to enhance financial inclusion.

Borrowing a play from the Reserve Bank of India’s playbook, the CBN is exploring the introduction of a new bank model — Payment Service Banks (PSB).

What is a Payment [Service] Bank?

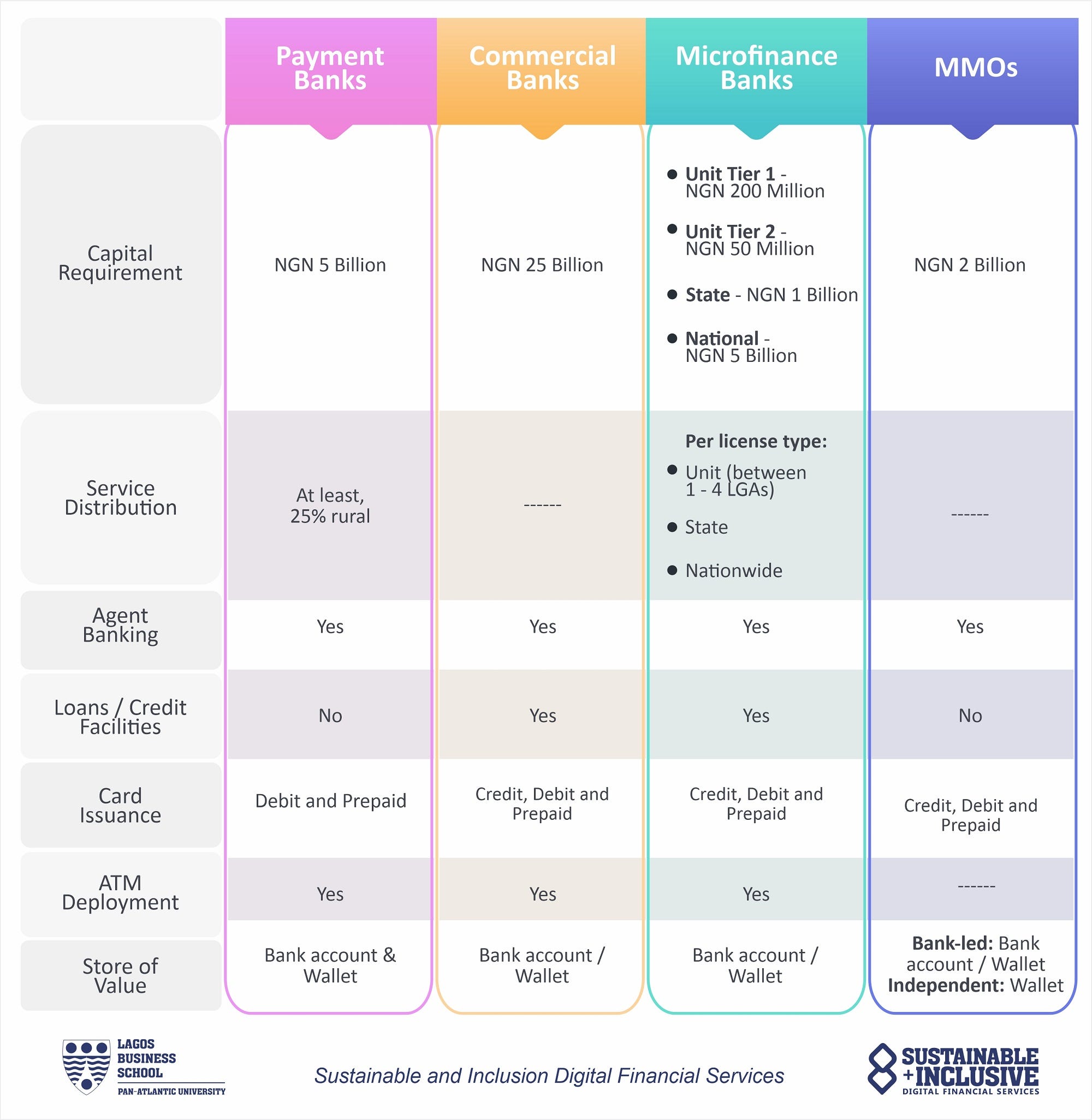

The Payment Service Banks (or simply Payment Bank as they are called in India, is a new category of bank with smaller scale operations and the absence of credit risk and foreign exchange operations. In addition to accounts (current and savings), PSBs can also offer payments and remittance services, issue debit and prepaid cards, deploy ATMs and other technology-enabled banking services. Think of them as basically stripped-down versions of our traditional deposit money banks, with limited functionality and a focus on onboarding more of the excluded and marginalised population.

Subsidiaries of mobile network operators (aka telcos), mobile money operators, retail chains (supermarkets) and banking agents are welcome to apply for the PSB license, provided they can meet certain requirements, including a 5 billion naira capital base, and a combined 2.5 million naira application and license fee (which are non-refundable).

A Brief History of Payment Banks

India’s high unbanked population has been the subject of much discourse, locally and internationally. In a bid to reduce the number of Indian citizens without bank accounts, the Reserve Bank of India (RBI) began exploring different interventions. The concept of Payment Banks was first introduced in 2013 when a committee on Comprehensive Financial Services for Small Businesses and Low Income Households was formed, and the committee recommended a new bank category called Payments Banks.

In 2014, invitations were sent out for interested parties to apply. The following year, the RBI granted licenses to 11 applicants, despite receiving a total of 41 applications. Of the 11 licensed PSBs, 3 have surrendered/given up their licenses, while 6 PSBs have commenced operations, albeit only 4 are prominent.

What differentiates a Payment Bank from other Financial Service Providers?

One peculiarity of PSBs is they are not permitted to offer loans or credit facilities to their customers — they can only receive deposits. Thus, Payment Banks cannot entirely replace traditional Deposit Money Banks, but they can serve as intermediate providers of financial services to new customers.

Payment Banks can issue debit cards but not credit cards. Also, unlike traditional banks, you can keep a limited sum in a payment bank account. Payment Banks offer interests on customer deposits, though the rate of interest is still unknown/yet to be decided.

Unlike deposit money banks (DMBs) and microfinance banks (MFBs), from day one, PSBs have a heavy reliance on technology via digital financial services, complemented with a strong agent banking model, which is meant to reduce overhead costs.

>> On September 18, 2019, the Central Bank of Nigeria issued Approvals -In-Principle (AIPs) to Hope PSB, Money Master PSB and 9PSB to operate as Payment Service Banks (PSBs).

>> On August 28, 2020, the Central Bank of Nigeria granted full licenses to Hope PSB, Money Master PSB and 9PSB to operate as Payment Service Banks.

What impact will this have on financial inclusion? Could this be the magic bullet we have been waiting for? How disruptive will this new entry be and what impact will it have on the entire ecosystem in general?

Updated Guidelines

Between 2018 when the first guidelines were released and Q3 2020, when PSBs were granted final licenses, the guidelines have been reviewed and updated in the following ways:

- Switching companies are now included on the list of entities that can apply for and operate a PSB license.

- To enable fair competition, the parent or associated entities of a PSB are forbidden from discriminatory or differential pricing in products and services offered to other PSBs and CBN licensed institutions. (This had been implied in the old guideline but has been emphasised with more detail).

- PSBs are to interface with the Nigeria Inter-bank Settlement System (NIBSS) platform in order to promote interconnectivity and interoperability.

- Rate of charges: PSBs are to adhere to the CBN’s Guide to Charges by Banks, Other Financial and Non-bank Institutions.

KYC: A Potential Bottleneck

The new guideline states that PSB customers under the tier-1 account category shall require name and phone number as identification requirements. If this translates to tier-1 account holders requiring only these two elements to fulfil KYC requirements, it gives momentum to the onboarding process.

However, some stakeholders anticipate that this may cause some problems in the near future especially if the CBN mandates PSB account holders in all KYC tiers to have BVNs as it did with commercial and microfinance banks.

If you recall, in 2017 when the CBN reviewed the KYC requirements for mobile money wallets, it also clarified that mobile money wallet holders on KYC tier-1 are not required to provide a Bank Verification Number as part of the KYC documentation.

The need may arise once again for further clarification on whether PSB customers with tier-1 accounts require a BVN (or not).

Are PSBs the Magic Bullet?

The objective behind the licensing of PSBs, according to the CBN, is to “enhance financial inclusion by increasing access to deposit products and payment/remittance services to small businesses, low-income households and other financially excluded entities through high-volume low-value transactions in a secured technology-driven environment.”

In business terms, we could say the entry of PSBs into the market is to further the digitisation of the financial ecosystem at the bottom of the pyramid & the informal sector, which is where most of the excluded population are. This gives PSBs the opportunity to become the primary champions of financial inclusion for those customer segments.

There’s obviously a lot of excitement in the financial inclusion space (we’re excited too) and the next few months should be interesting.

Challenges

The existence of PSBs is not without its own set of challenges. These include:

— Revenue model (earning potential): the inability of PSBs to lend/give credit limits their earning potential.

— High competition: even though electronic payment systems are still nascent to underserved customers, the competition with cash would require behavioural change that would enable a truly cashless society.

— Irregular saving pattern among target segment: there’s limited knowledge of the savings patterns and profiles of the underserved; hence, PSBs will need deep understanding of their market segments to enhance and deploy product-market fit.

— Infrastructure: the nationwide availability of power, telecoms and other requisite infrastructure may increase the cost of PSBs and reduce their reach.

— High setup and operational costs.

— — — — — –

Want more insights on PSB profitability and customer adoption? Read next: 4 Important Takeaways from the Payment Service Bank Webinar